In order to examine the Incentive Zoning (IZ) Program, the city hired analysts to model some different outcomes based on various assumptions. The analysts were trying to tease out how different structures of the program would affect affordable housing in the city. Ultimately, a 43-page report was published by the analysts to tackle the issues surrounding the city’s IZ program.

The background

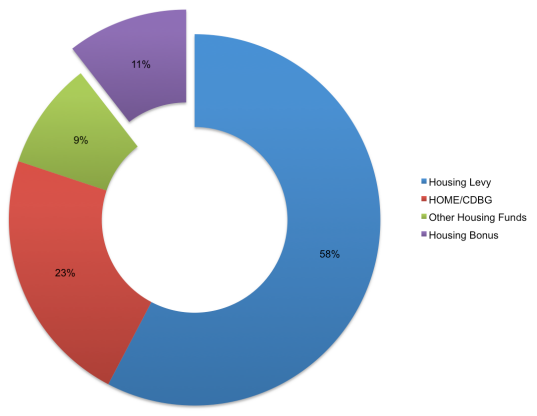

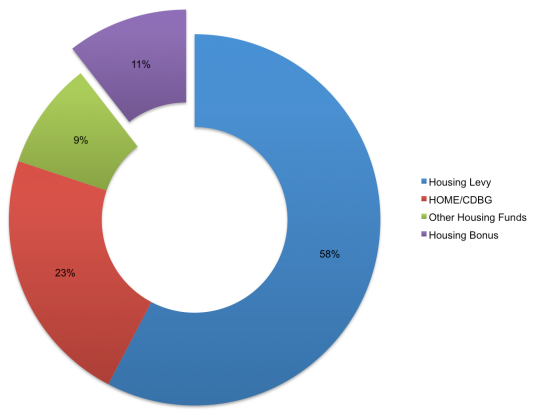

The incentive zoning program has been in place since 2001 and affects particular zoned areas in Downtown and South Lake Union. The program is structured so that developers can get certain advantages, such as increased height if they build affordable units in their structure or pay a fee. Over the 13 years since the inception of the program, analysts found that it produced 714 units of affordable housing. Overall, the program makes up 11% of the total funds for affordable housing.

The analysts’ task

To be clear, this is not an analysis of the best way to make housing affordable in Seattle. Instead, this is an analysis of whether or not it is possible to increase the production of affordable housing under the IZ Program–an important distinction. John Scholes who commented on behalf of the Downtown Seattle Association noted that the analysts said it would be difficult to significantly grow the program, and even if it were doubled, it would barely put a dent in the need for affordable housing. In other words, the report shouldn’t be viewed as an attempt to tease out a solution to the affordable housing problem, instead it is only an attempt see potential impacts of the IZ Program.

The surprising findings

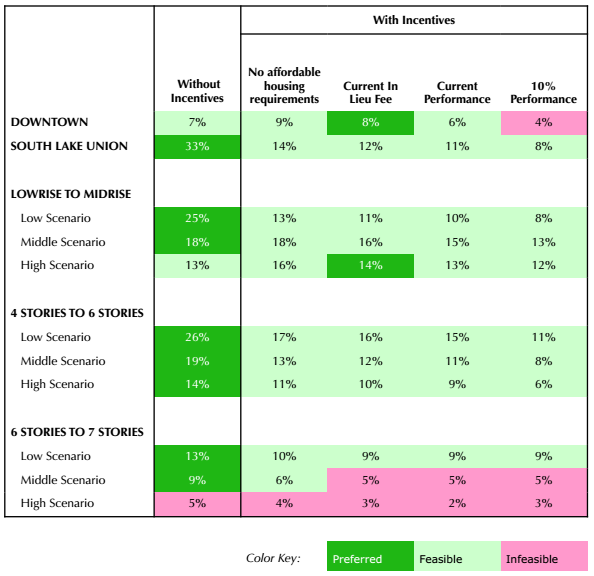

The image below forms the basis for most of the report. Essentially, the analysts wanted to tease out different potential returns on development under various scenarios. As an example, the ‘middle scenario’ of low-rise or mid-rise development that doesn’t utilize the incentive zoning programming shows an 18% return. Returns in red indicate development that is unfeasible while those in light green indicate the development is feasible.

The analysts assumed that if the return on development is 5% or more, developments are considered feasible, while those under 5% are not. As you can see, the study indicates that development is feasible under nearly all the different scenarios. In this sense, the study would lead people to believe that fees could be raised on nearly all private development and developers would still make a profit. This implies that they would continue to build housing, but our understanding deepens with the most important finding by the analysts.

In this analysis, the darker green highlights the most preferred type of building. What it shows us is that in nearly all scenarios, the most preferred option is not utilizing the incentive. Regardless of whether or not the numbers are accurate, this shows the logic of developers. It doesn’t matter whether or not they can still be profitable after paying a fee. Instead, it matters what options they are going to choose given the costs of various options.

This basically means that you can’t simply offer incentives to developers, like upzoning, if the costs of those incentives make them less profitable. Specifically, the 6-7 story buildings show the lowest returns and are the only building types that become mostly unfeasible (disregarding whether they are preferable) under the incentive zoning program. In other words the program is most at odds with building types that help walkability, transit, density, environmentalism, lowering the per capita cost of city services, sustainability, and much more.

Recommendations

From these observations, a number of recommendations were made. The analysts were careful not to say that Seattle shouldn’t pursue the IZ program. Instead, they indicated how the money could be used better by by focusing on the right income groups, making sure incentives don’t discourage high-density development, increasing the amount of funding that goes to particular housing types, and more. In addition, the analysts made an unexpected recommendation. They indicated it would be worth studying the impact of converting the program from an incentive zoning program to a linkage fee program. Specifically, the analysts would like the city to commission a Nexus Study to better understand the impacts of linkage fees.

Questions

I think the study shows a lot of great work and is exactly the type of effort we need from the city. With that said, I think we can learn a lot about pursuing future studies. There are a number of critical questions left unanswered. If the city pursues the IZ program or decides to study linkage fees, I think it’s important that the following issues are addressed:

- Are there programs that could have bigger impacts? Council Member Clark acknowledged that the results from this program may seem small, but they are still important. There is no doubt that all affordable housing has real impacts, affecting people with important needs. It is also important to acknowledge that we face opportunity costs. If we spend all our time and effort working on a program with a small impact we may be missing programs or ideas that have much larger impacts. The city has spent nearly equal time studying the IZ program as it has studying numerous alternative options and there are even more programs that haven’t been examined at all. If a better alternative is found, the time, money and housing lost that could have been used studying another program is opportunity costs.

- How do Incentive Zoning or Linkage Fees affect the larger housing market? It’s fine to tailor a program to raise more money, but the ultimate goal is to lower everyone’s housing costs in addition to ensuring everyone has affordable housing. It is entirely conceivable that increasing the production of affordable housing by one program could consequently negatively affect overall housing costs. In fact, some attendees asserted the study indicated this was already happening.

- Are these scenarios accurate? There are a lot of assumptions being made. Determining return on investment is fraught with unknowns. It requires guessing future rents, land values, development costs and much more. Additionally, I see some of these numbers extremely skeptically. Indicating 33% return on equity requires further scrutiny. It’s one thing for a model to produce this estimate and entirely different for evidence from actual development to show that.

Owen Pickford

Owen is a solutions engineer for a software company. He has an amateur interest in urban policy, focusing on housing. His primary mode is a bicycle but isn't ashamed of riding down the hill and taking the bus back up. Feel free to tweet at him: @pickovven.