Seattle is pursuing an inclusionary zoning policy called Mandatory Housing Affordability (MHA), similar to successful programs in over 500 municipalities, including Redmond and Federal Way. However, it’s not without critics. Dan Bertolet, the lead housing writer at Sightline, is one of those critics. He recently wrote two harsh articles along with three other criticisms1, 2, 3. This shouldn’t come as a surprise. Bertolet’s background includes opposing various forms of inclusionary zoning over the last few years; at Crosscut, Smart Growth Seattle (a lobbyist for developers) and his own blog City Tank where criticism was focused on a voluntary program4, 5, 6, 7, 8, 9.

Before diving into the details, it’s worth considering the big picture. Sightline created hypothetical projects threatened by MHA, then extrapolated this to suggest housing supply will decrease, rather than other possibilities, such as developers pursuing different projects. While MHA aims to produce 6,000 affordable homes, the articles don’t address the magnitude of impact on housing supply. On the other hand, empirical research10, 11, 12, 13 and expert opinion suggests minimal or no impact on housing supply. Some research even finds inclusionary zoning increases housing supply.

The Feasibility Question

There’s also ample reason to doubt Bertolet’s hypothetical examples would be threatened by MHA. He says,

In practice, developers usually apply a more complex pro forma, but again, because for MHA the important result is the before-and-after difference in return, a simple pro forma is sufficient here.

The return on investment (ROI) before and after MHA doesn’t predict the policy’s success. A project with a 50% ROI before MHA and 20% after would have a shocking 30% decline in ROI! Yet, both scenarios are feasible. Bertolet later says,

For the proposed upzone from NC85 to NC95, MHA would actually obliterate almost all of the return on investment.

This doesn’t refer to the difference in ROI, only the near zero ROI after MHA. It may be unintentional but readers are left with the impression his number reflects feasibility. This moves the goalposts from his original claim.

In sum, Bertolet’s argument consists of a simplified pro forma not meant to indicate feasibility and no overall market analysis. Fortunately we have more robust analysis, indicating MHA is feasible. Most people concerned about housing supply can stop here.

However, readers interested in the minutiae of Bertolet’s numbers will also find those questionable. He declined to share his spreadsheets but a close approximation is reproduced in these four spreadsheets. The following screenshots capture variations from those spreadsheets. Overall, there are two categories of problems: missing calculations and problematic assumptions.

Missing Calculations

First, there are no loan details in these scenario. Developers doing $45+ million dollar projects will use loans. The first example, NC-65 to NC-75 with on-site MHA, shows a low 8.3% ROI. However, investor returns on equity would likely be 15-20%.

Second, Bertolet leaves out important feasibility calculations. For example, do projects produce enough income to get loans? This is often determined with a debt coverage ratio (DCR). All of his ‘before MHA’ scenarios would likely not be able to receive large enough loans with a DCR of 1.25. If projects aren’t possible without MHA, it’s not surprising they’re infeasible with MHA.

Third, it’s not instructive to focus on a small set of hypothetical projects. All four examples begin with an ROI of 13%. These scenarios show projects on the edge of feasibility. MHA might make some hand-picked examples infeasible but it doesn’t matter if other examples become feasible and the overall impact is minimal. For example, the lot at 1202 NE 50th St would likely see an increase in ROI after the University District rezones.

Bad Assumptions

Bertolet’s entire argument also rests on some highly variable assumptions.

First, recent industry research suggests Bertolet’s capitalization rates might be wrong. This number dramatically impacts ROI. Below are examples from adjusting capitalization rates only half of one percent.

Second, Bertolet assumes developers are inflexible. His examples show a single scenario that is problematic but doesn’t illustrate changes developers might make. Some possibilities include decreasing unit sizes, reducing parking, or avoiding additional concrete by using more FAR in a shorter building. Bertolet’s example of NC-85 to NC-95 in a medium market, additional FAR from MHA (6.25 compared to 6) could be used in a 85-foot building, keeping the same construction costs. This makes the MHA option feasible.

The Bigger Picture

Without government intervention, regardless of the housing supply, housing markets will segregate by income. Amid the discussions of feasibility and growth, it’s worth remembering that equity requires inclusionary zoning. A city must have affordable homes in all neighborhoods. Seattle’s MHA program requires most new development contribute towards neighborhood affordability.

Bertolet’s writing continually focuses on regulatory costs. All this quibbling over small changes in costs misses the forest for the trees. The biggest problem Seattle has control over is density, not regulatory costs. While MHA would make up only 3-8% of total project costs, it also increases density.

Bertolet focuses on regulatory costs while land prices rise, often account for over 20% of total costs. Labor prices are also rising dramatically. Yet we’re in the middle of a record-breaking apartment boom. Focusing on regulatory costs implies we can’t have a nice city with energy-efficient buildings or seismic retrofitting. Instead, regulations must make real estate the most profitable investment. But maximizing returns to real estate sets us up for failure. We need to make sure development is feasible and regulations ensure construction booms create affordable housing.

Since affordable housing advocates know this, they began working on inclusionary zoning nearly 20 years ago. Slow and fitful progress was opposed by Bertolet and others prior to the most recent construction boom. If opposition hadn’t prevented faster implementation of a more ambitious program, a 10% requirement might’ve netted Seattle about 3,000 units.

Regardless, Seattle’s recent breakthrough resulted in MHA legislation that is awaiting implementation. This legislation is the result of a multi-year stakeholder engagement. It builds upon consistent empirical research and a general consensus among housing experts.

In consultation with housing experts, stakeholders outlined specific details for Seattle’s program:

- 3-10% of all new residential units should be affordable;

- A developer fee is required equal to the subsidy cost plus 10%, if units aren’t built on-site;

- The requirement will apply to Seattle’s 28 urban villages and urban centers; and

- Areas will be rezoned to ensure development creates affordable housing.

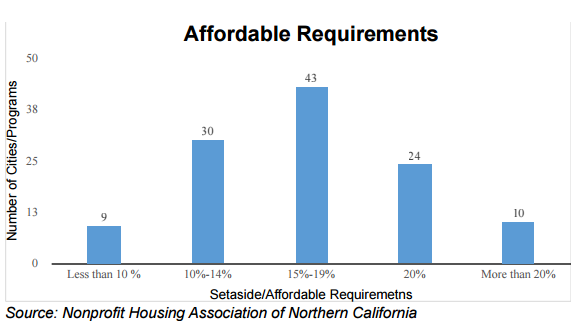

These details in context of academic research suggests Seattle’s program is conservative:

- Hot housing markets with inclusionary zoning typically require 10-20% affordability; and

- The first finalized zoning proposal shows large capacity increases.

Wrong Questions, Misleading Answers

Bertolet’s strategy to focus on marginal examples, using bad assumptions, is a pitfall of the pro forma analysis. Like a restaurant owner opposing a minimum wage increase because their accounting shows it won’t work, Bertolet’s analysis relies heavily on specific assumptions without acknowledging the flexibility of markets. A proper analysis was already completed in a number of studies14, 15, 16. That effort echoed what’s found in the academic research; Seattle’s MHA won’t affect housing supply.

While this article focuses on criticizing Sightline’s articles, it’s possible Bertolet is right and the affordability levels are too high. Since he didn’t share his calculations, they are recreated them for readers to play around with themselves. However, it’s also possible that the MHA requirements are too low. Nico Calavito, a housing expert involved with inclusionary housing implementations, summed this up, “It seems to me that with an upzoning 3-10% [inclusionary requirement] is a very small amount. If upzoning is involved it should be higher than that.”

Fortunately, the law requires the program to be reviewed, allowing us to alter the numbers if necessary. Bertolet paints a grim picture but the reality is much less concerning. Lower housing supply is only one, unlikely outcome of many possibilities. Developers may adjust their design, wealthy renters might pay more, labor costs can decrease and developer profits might go down. Bertolet also continuously overlooks the most likely outcome, despite the evidence, of an incorrect MHA requirement; land prices will change. Yet his own examples show land prices adjusting to construction costs.

Frustratingly, Bertolet calls for the city to conduct further feasibility analyses. This is the same strategy used by density opponents trying to block the University District upzones. Some are even referencing Sightline while opposing upzones. Density advocates are feeling discouraged and less likely to advocate for MHA upzones, handing the megaphone to opponents. The only result of all this will be less density and less affordable housing.

In a city that has the most cranes per capita and some of the fastest climbing home values, it’s high time we mandated equity. This construction boom won’t last indefinitely and we need more homes for our growing population. At a time when our nation is fighting over whether to close our doors on refugees and immigrants, we have to keep our priority front and center; opening Seattle’s doors to people of all incomes, races, nationalities, and religions. That doesn’t require us to just build; it requires us to build justly.

The Seattle Process has done its job. Now is the time to move forward with MHA. The need has never been greater.

Editor’s Note: A correction was made to the LR3 to NC75 upzone image. The wrong MHA percent was used in the original assumption.

Footnotes

- http://www.sightline.org/2017/01/10/checking-seattle-mandatory-housing-affordability-math/

- http://www.sightline.org/2016/06/01/seattles-housing-future-depends-on-a-mathematical-and-political-balancing-act/

- http://www.sightline.org/2016/11/29/inclusionary-zoning-the-most-promising-or-counter-productive-of-all-housing-policies/

- http://citytank.org/2013/10/23/welcome-to-the-affordable-housing-policy-twilight-zone/

- http://citytank.org/2013/10/15/the-road-to-san-francisco-is-paved-with-housing-supply-suppression/

- http://citytank.org/2013/09/26/we-should-all-be-on-supplys-side/

- http://citytank.org/2013/10/31/the-mixed-messages-and-misplaced-burden-of-taxes-on-new-development/

- http://citytank.org/2013/11/22/getting-real-about-the-costs-and-benefits-of-affordable-housing/

- http://citytank.org/2012/12/05/density-shrugged/

- http://furmancenter.org/files/publications/IZPolicyBrief.pdf

- http://onlinelibrary.wiley.com/doi/10.1111/j.1467-9906.2010.00495.x/abstract

- http://www.huduser.org/portal/periodicals/cityscpe/vol11num2/ch1.pdf

- http://www.wellesleyinstitute.com/wp-content/uploads/2013/01/Rosen2004.pdf

- http://clerk.seattle.gov/~public/meetingrecords/2014/plus20140930_9d.pdf

- http://www.seattle.gov/Documents/Departments/HALA/Policy/2016_1129%20CAI%20HALA%20Economic%20Analysis%20Summary%20Memorandum.pdf

- http://clerk.seattle.gov/~public/meetingrecords/2014/plus20141014_1d.pdf