How Federal Subsidy of Loan Interest Rates Block Missing Middle Housing

Earlier in the pandemic, I was searching around Zillow. Looking at houses was a fair alternative to doomscrolling Reddit. One evening, I came across a building for sale. Interesting place in our neighborhood with a couple apartment units and my car parked out front. Our landlord put our house on the market.

Thankfully, I don’t need to be worried about immediate housing. Our landlord is a gem and our lease goes for a while, so we’re secure regardless of ownership. The building really is just a few units, built as a small apartment building in the 1970’s. It’s not where I expected to spend forever, but the opportunity made me wonder if we could afford to buy the place.

The long and the short is no. The price was high for what we could afford, even with renters contributing to the monthly mortgage. But the process of getting to that firm no was an interesting one and it shows some of the rarely discussed hurdles to expanding and maintaining the city’s multifamily housing stock. We all know that Seattle’s zoning is segregationist, the permitting process is frozen molasses, and construction prices are sky high. Even before that point of building new, it can be hard to keep the existing multifamily units we have because there’s not a lot of options for financing them.

Conventional and Jumbo and Vocabulary

Like most people looking to buy a house, my first call was to my bank. We’re in pretty good standing with a couple of credit unions. I was surprised to find out that none of them actually write mortgages for three- and four-unit buildings. Our credit unions top out at duplexes.

So, on to the commercial banks. The commercial banks were willing to write a mortgage for up to four-unit buildings, however they had very strict limits on the loan amounts. We would have to come up with a half-million dollars to get under the limit. At about a third the price of the building, it was slightly more than the downpayment we were expecting. This was more difficult to hear because the same banks would finance a single-family home of equal size and higher price at a much lower downpayment.

Which landed us on the phone with Jon Wagher, Senior Loan Consultant for Caliber Home Loans and very patient explainer of residential mortgage financing. Jon took the time to go into why many banks will not write a “jumbo mortgage” for houses other than single-family homes.

Jumbo mortgages are simply loans that are above the limit where the law restricts purchases by Fannie Mae and Freddie Mac. This is the point where we are going to have to get into all of those mortgage terms.

About a third of mortgages in this country are government backed loans. These are mortgages that are guaranteed by the federal government through the Veteran’s Administration, the Federal Housing Administration, or the United States Department of Agriculture. There’s specific rules in each program including veteran status, low income, or if the land is going to be farmed. Banks set up these mortgages so it can get confusing, but the important part is that the federal government is guaranteeing that they’ll be paid off.

Loans not directly insured by the federal government are called conventional loans. These mortgages are between you and a bank. You come to the table with collateral, income, and the house you want to buy. The bank comes with cash to buy the house and a stack of paperwork for you to encumber your life for the next 15 to 30 years.

But the feds are still involved, particularly in one flavor of conventional mortgages called “conforming” loans. These loans conform to the limits set up by the Federal Housing Finance Agency (FHFA). If a bank writes a conforming mortgage, they can then turn around and sell that loan to Fannie Mae and Freddie Mac — the federal mortgage loan companies. The bank can then use the money they receive to write more loans. Conventional loans keep cash moving in the economy.

How much is the limit for a conventional conforming loan? FHFA divides the country up into low- and high- cost areas. Seattle falls in the second category, unsurprisingly. For 2021, the FHFA limits are:

| Building Size | FHA Maximum | FHA Maximum High-Cost Areas (King County) | FHFA Conforming Maximum | FHFA Conforming Maximum High Cost Areas (King County) |

| One Unit | $356,362 | $822,375 | $548,250 | $776,250 |

| Two Unit | $456,275 | $1,053,000 | $702,000 | $993,750 |

| Three Unit | $551,500 | $1,272,750 | $848,500 | $1,201,200 |

| Four Unit | $685,400 | $1,581,750 | $1,054,500 | $1,492,800 |

Federal loan limits comparing non-conventional and conventional loans. FHA loan limits are for loans subsidized by the federal government. FHFA limits are for conventional conforming loans sold by banks to eventually be resold. (FHA, FHFA)

Such a national system “is great,” says Wagher. “It creates a predictable standard for guidelines and ‘smooths out’ the regionality of interest rates.” FHA loan rates are so predictable that they talk about changes on the evening news. According to Nerdwallet’s daily average rate tracker, a 30-year fixed conforming conventional mortgage right now is 2.8%.

Jumbo mortgages are simply loans over FHFA limits. They cannot be sold to Fannie Mae or Freddie Mac, so the loan is an investment of the bank and stays on the bank’s portfolio. To qualify, the mortgagee needs great credit, a solid down payment, and certain income levels compared to the size of the loan. According to Wagher, this is the private sector stepping in where Fannie and Freddie are limited.

Companies like Caliber Home Loans who have their own portfolio can also write jumbo loans with creative terms, such as using other assets as collateral. But that comes at a risk, and in financing, increased risk will increase the mortgage’s interest rate. There lies the problem.

As Wagher puts it, “everyone wants ultra-low rates, but doesn’t see what must be sacrificed to get them.” That 2.8% rate has given the country an unreasonable image of what it costs to own a home. Everyone is so used to the cheap interest rates that are partially paid by the federal government. More expensive rates come as a stunner, even if the higher price means higher quality or better service. In the case of jumbo mortgages or mortgages that calculate rent as part of the income, the service is long-term risk staying on the lender’s books for the life of the loan. The ubiquitous talk of low rates turns other forms of financing into niche items. “Because consumers don’t want to pay the high rates,” says Wagher, “lenders aren’t willing to invest the resources to create the products.”

Interest rates are directly tied to risk. While Fannie and Freddie don’t guarantee a loan like the VA, they subsidize the low interest rate by spreading the risk across many other parties. It’s a mechanism that many consumers simply don’t see. Wagher is sympathetic to the position many buyers are in. “Consumers are constantly marketed to. ‘Low rates, act now before it’s too late!’ But, often the context is lost in the fine print.”

What’s so great about triplex and quads?

Triplexes and quadruplexes — three-unit and four-unit buildings respectively — are the cornerstones of “missing middle” development. While they may not be a panacea, they make for eclectic neighborhoods of comfortable density.

Admittedly, I have a soft spot for the form. I lived in Montréal for a number of years, and the basic house of The Plateau is a townhouse triplex. First floor door at the street went to one apartment, usually the owner-landlord. Curling outdoor stairs to a second floor balcony and two doors. One went straight into an apartment and the second to another set of stairs upward. Local legend said the unique stair design was because the Catholic Church frowned on shared indoor spaces.

The building looks like a nice brownstone, one of the benefits of triplex and quads. They don’t take up more space than a single-family home but they make room for triple the number of households. Such homes put enough people in the neighborhood to warrant groceries and really good bagel places. They’re also builders of generational wealth for immigrant families. One family’s investment can make space for distant relatives, newcomers, setting up independent children, and then eventually be available for college kids trying to finish their urban planning graduate degree before their visa runs out.

Such a generational wealth story echoed in my own family in a slightly different form. My maternal grandparents owned a home in suburban Maryland that evolved over the years into a defacto triplex. Starting with a Cape Cod style house bought on a VA loan, my grandparents added a mother-in-law suite and a second floor apartment. At some point in all their adult lives, every aunt and uncle (Catholic family, there’s lots) lived in one of these accessory homes. More than outright cash, the home’s flexibility was crucial. It’s the kind of financial stability that doesn’t often appear in our current housing market.

First Problem: The Cost Gap

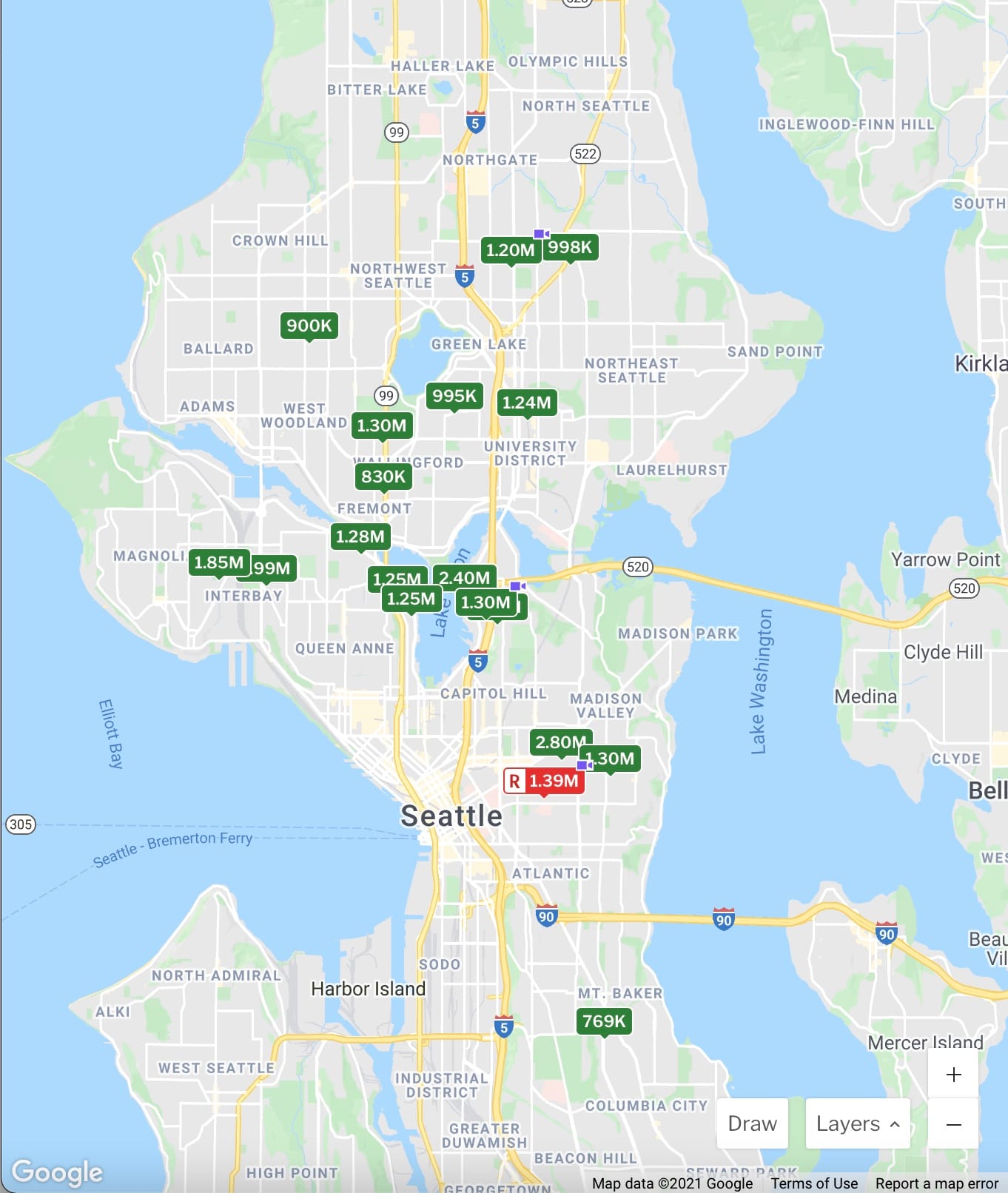

The median home price in Seattle for May 2021 was $818,750. Of the 1,368 homes sold in Seattle during that one month, 684 of them went for more than $818,000, and 684 sold for less. That figure is $42,000 or 5% more than the absolute limit for conventional conforming single-family loans. Our housing market is bonkers.

It may be surprising that FHFA does include multi-unit dwellings in its rules. In King County, a triplex can be purchased for $1.2 million and a quadruplex for $1.4 million and get all of those low interest rate incentives available to conventional conforming mortgages.

If we look at the actual buildings available, it’s more difficult. Of the 16 Seattle triplexes that were for sale in a recent Redfin search, only six were available for less than the loan limit for three-unit buildings. The remaining ten were above the FHFA threshold. (One was actually two neighboring triplexes for sale for $2.8 million. Which would put each of the buildings above the FHFA limit.)

But let’s look at this another way. Seattle’s lots can fit three to five townhouse units on them. Each of those houses sold for the $776,000 county max for single-family homes, replacing a triplex with three townhomes would gross the developer $2.3 million. So if we’re talking about working within the FHFA loan limits why would someone tear down a single home and build a $1.2 million triplex when they could flip it for three townhomes that can be sold for a million dollars more? The high limits for single-family homes compete directly with financing multi-unit developments.

The Second Problem: Lack of Clarity

At the time of the 2008 mortgage bubble, sub-prime loans were marketed as a mechanism to get more people into homes of their own. The requirements for the loans were lowered in ways that changed the risk, but expanded the number of people that qualified. In retrospect, the dangerous mechanisms that went into changing that risk — balloon payments, rigging applications, and predatory targeting of customers — were overshadowed by the goal of getting people into houses.

So if we want to work out this current housing crisis without it becoming another mortgage crisis, understanding the way lenders put a price tag on risk is vital. It allows us to discuss expanding the types of mortgages and who they are available to, while avoiding another three-card-Monty game like the one that led to the 2008 collapse.

Instead of cloaking a mortgage in terms of art like “conventional conforming” or “jumbo”, we can start talking in plain language. That would open up the discussion to regular people and knock 500 words out of articles like this. If a loan is structured to get traded by Fannie and Freddie, just put their name out front and make it obvious. And like with health and politics headlines, the nightly news can do a much better job on depth and avoid talking about interest rates like hockey scores.

The flip side, consumers must get a grip on our expectations. That VA mortgage my grandparents got for their Maryland home was 18% on $10,000. By focusing on low rates, we miss asking why conventional mortgage rates are so low. When most people can’t qualify for a loan that banks then make extra money shuffling around, is the system working? We can’t even talk about whether this is the economy we want because too few folks make it past the introduction.

The Third Problem: Few Products

Once we’re ready to plainly talk about how federally subsidized risk produces market flooding low interest rate products, we can start doing something about it. As Jon Wagher points out, the easy money of conforming conventional mortgages occupies such a huge place in the market that alternatives are boutique products. Jumbo loans are mechanisms for private banks and funds to step in the place of Fannie Mae and Freddie Mac.

One possibility is to lower the thresholds for conforming one- and two-unit mortgages. Counterintuitive, but it would take the federal government out of competition with multifamily dwellings. Alternately, the three- and four-unit limits could be raised to reflect the constrained, expensive land that allows multifamily developments. And, of course, local governments can drop the segregationist apartment bans.

Private mortgage writers do create alternative mortgages, but often they are bespoke one-offs. It’s far too difficult to find they exist, much less the rules and expectations. Just like I had to go through layers to get started is a ridiculous hurdle. And even then, it took referral from a friend — Sinead Keogh at Remax, if you need to buy or sell a house — just to get there.

No matter what, there needs to be more public mechanisms to spread risk. That may include public banks. It could also include public agencies that are sitting on huge sums of cash — and here I am looking directly at the University of Washington’s Endowment. Let’s be honest, public university endowments are simply public banks that are limited to spending their money on campus. A small expansion of “campus” would allow these massive pools of money to benefit the community that built the school. Public university endowments should develop a transparent, regular application to back mortgages for nearby residents building and maintaining neighboring multifamily buildings.

The Market has Mono

More than a specific act to correct the housing finance market, it is vital to recognize how many of these issues stem from the ubiquity of a conventional conforming mortgage. It’s a single use being tied to a single type of money being financed a single way. Just like fields of the same potato species can be wiped out in a blight and lead to famine, a housing market built around a single-family home paid for with fed-supported banks is leaving many people out of housing. Conventional conforming mortgages are a monoculture.

The way you return a monoculture to being a healthy system is through introducing alternatives. Infinite diversity in infinite combinations, as the saying goes. We can’t expect improvement by making everything identical. Trying to shoehorn six-unit apartments into the framework of conventional conforming mortgages would likely do more harm than good.

But we need to start somewhere. Families look different. Homes should look different. Why shouldn’t home financing keep up? Until it does, it will be a barrier to building an affordable city for many of those different households.

{kind=link}