Rumors of a slowdown were averted, but how long can Seattle keep it up with its permitting maze and restrictive zoning unsolved?

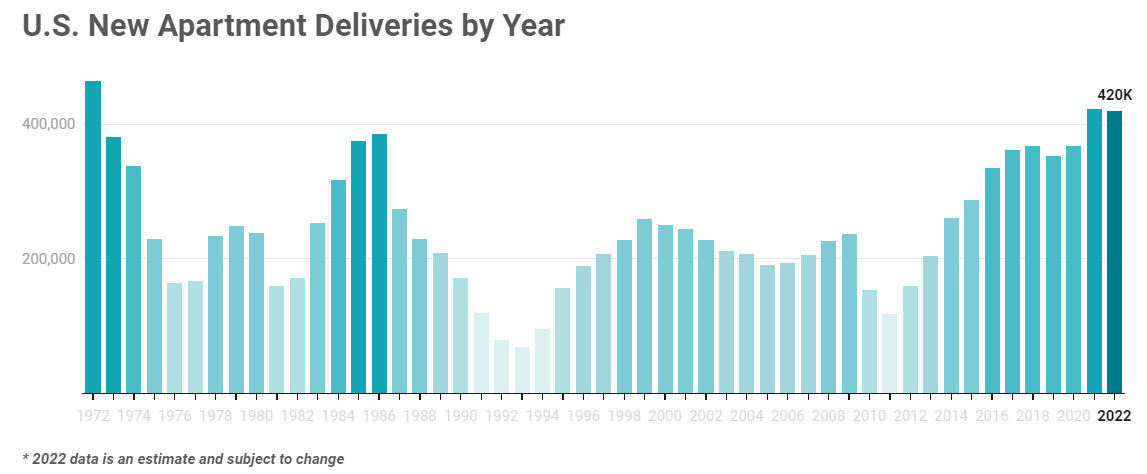

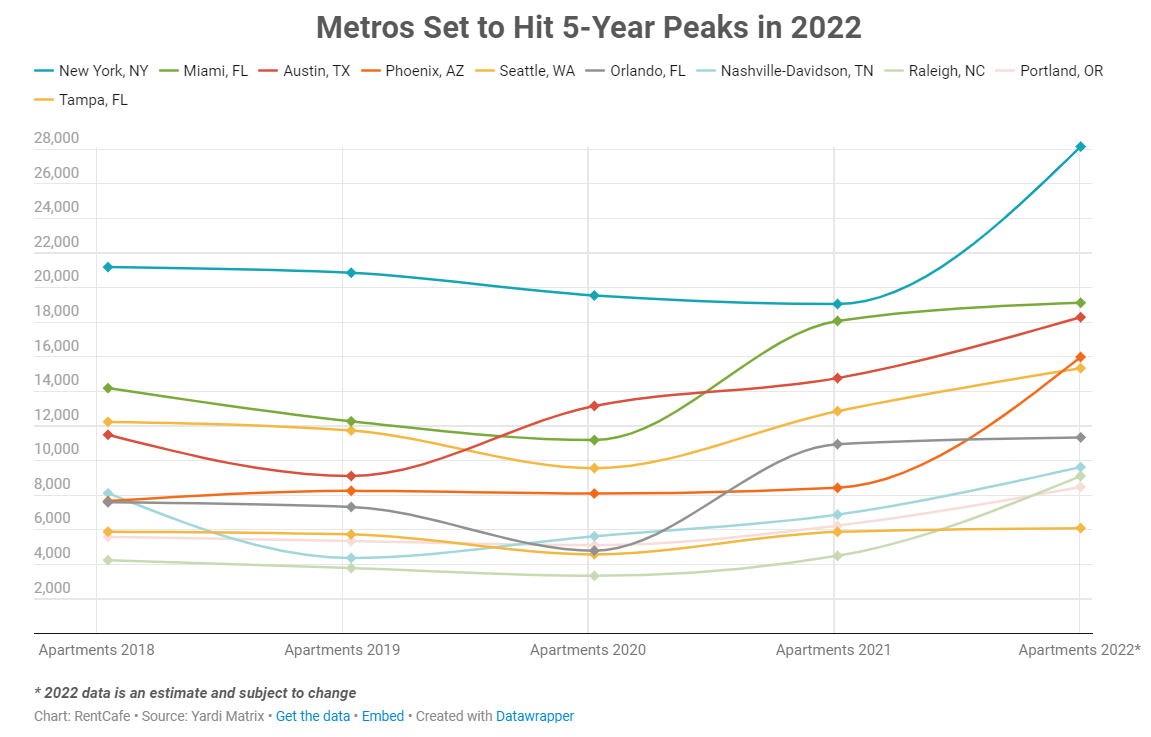

The pandemic has been tough on the construction industry, but apartment-building is showing signs of rebound, both nationally and in the Seattle metropolitan area. Multifamily construction is the midst of a 50-year peak in the U.S., RentCafé announced, with 420,000 new rental units expected to be completed this year. Seattle ranks seventh among U.S. metro areas in apartment production in those 2022 projections.

“Seattle Metro is firing on all cylinders on the development front, with 15,341 new apartments expected to hit the market by the end of this year,” RentCafé’s Michelle Cretu said in an email. “Construction rates in Seattle Metro are up by 19% compared to last year, when around 12,800 units were completed. That’s a very welcomed increase for many renters who are having a hard time finding a new apartment in this area.”

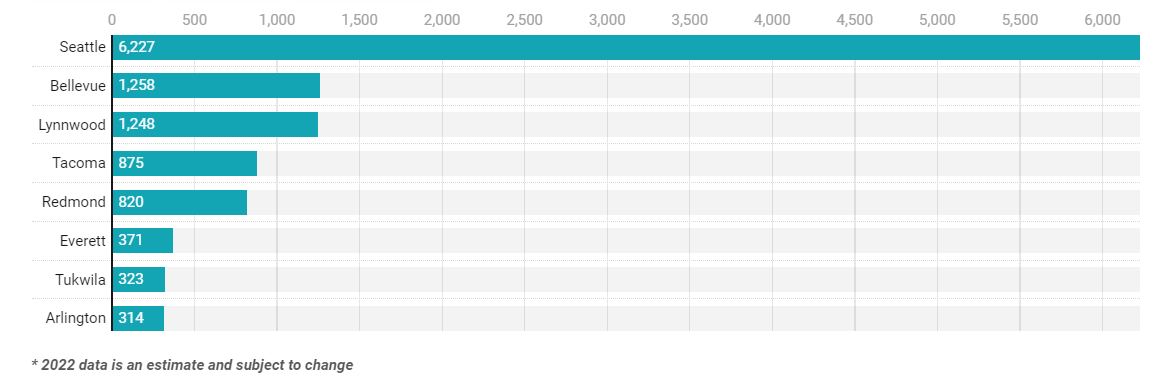

If projections hold, that apartment total would be a five-year high for the metro area, with the city of Seattle again far ahead of its neighbors at 6,227 new units expected by year end. RentCafé projects Bellevue will take second with 1,258 apartments and Lynnwood will take third 1,248 apartments added. Tacoma’s projection is 875 new apartments, which claims fourth.

“Current projections are placing Seattle Metro on track to hit a five-year record in apartment construction,” Cretu added. “In 2017, 13,350 new rental units hit the market, with completions steadily declining until 2020, when 9,561 units were built. By 2021, development picked up the pace again.”

RentCafé only tracks construction of apartment buildings with 50 or more units, so their report leaves out other forms of new housing, like small apartment buildings or condominiums and townhomes. Nonetheless, large apartment buildings increasingly compose the bulk of apartment production in the U.S. so the data provides a solid snapshot of what’s going on.

That rebound was somewhat unexpected as industry analysts were projecting a slowdown last year. One year ago, Rent Café had projected new apartment construction would be down by about 2.5% in 2021, with pandemic related slowdowns in permitting and financing, skilled worker shortages, and sky-high lumber prices all identified as factors contributing to the dip. That analysis was corroborated by data from Commercial Analytics, “showing contractors in the first six months of 2021 began building only a handful of projects, totaling 523 units,” Marc Stiles of Puget Sound Business Journal reported. “That slowing of construction starts could point to an even more abysmal 2022,” The Urbanist reported last August based on those reports.

However, 2021 ended up finishing strong and setting a new highwater mark, with 423,000 apartments added nationally. The Seattle metro added almost 13,000 in 2021, far exceeding RentCafé’s mid-year projections and its 2020 mark. In 2022, the Seattle region is on course to best this mark even with a four-month concrete stoppage that was hugely disruptive to the construction industry and still lacks a long-term fix as concrete companies refuse to meet union demands that would lead to a new contract being signed, threatening more stoppages to come.

Sunbelt continues to boom

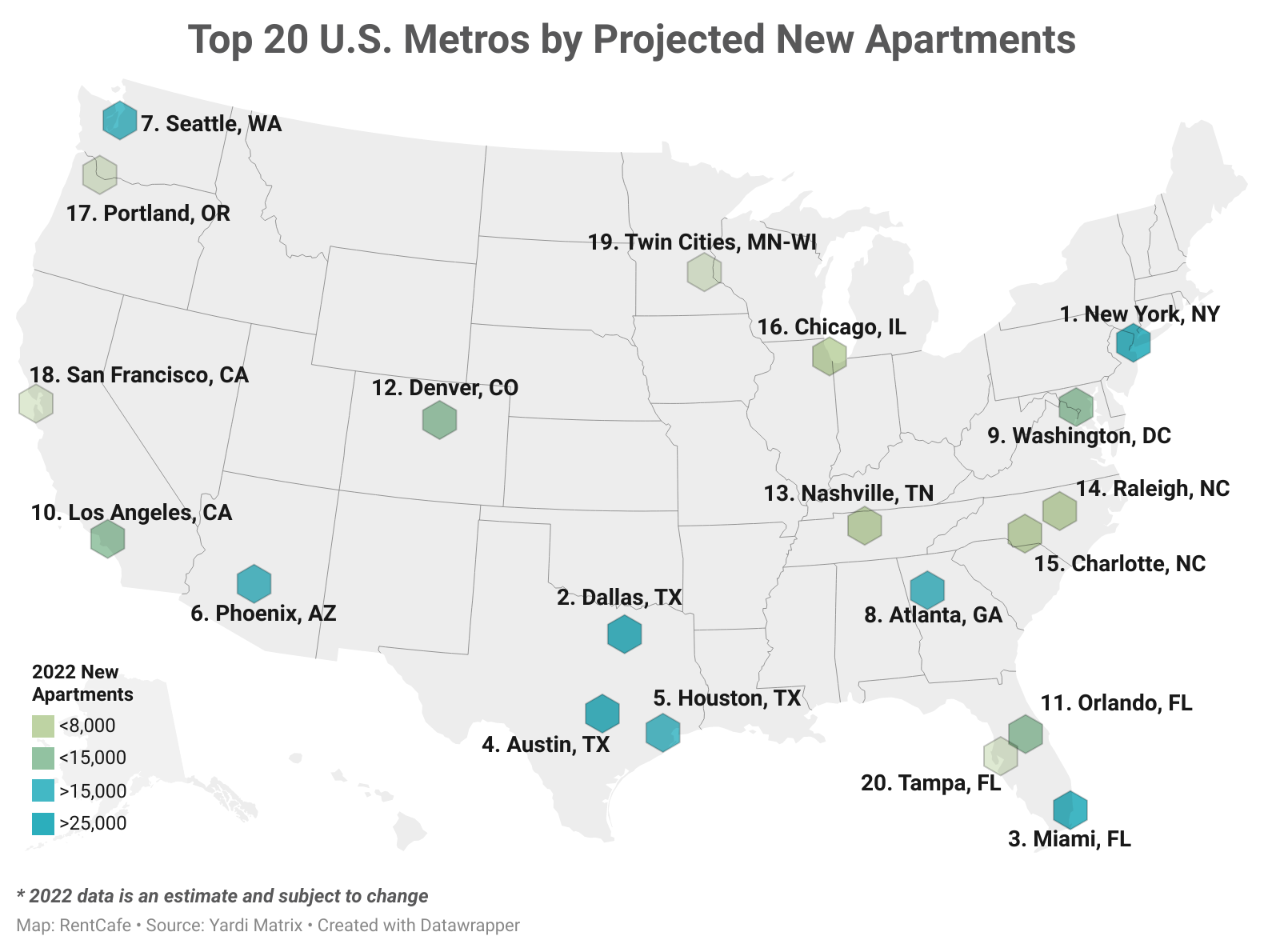

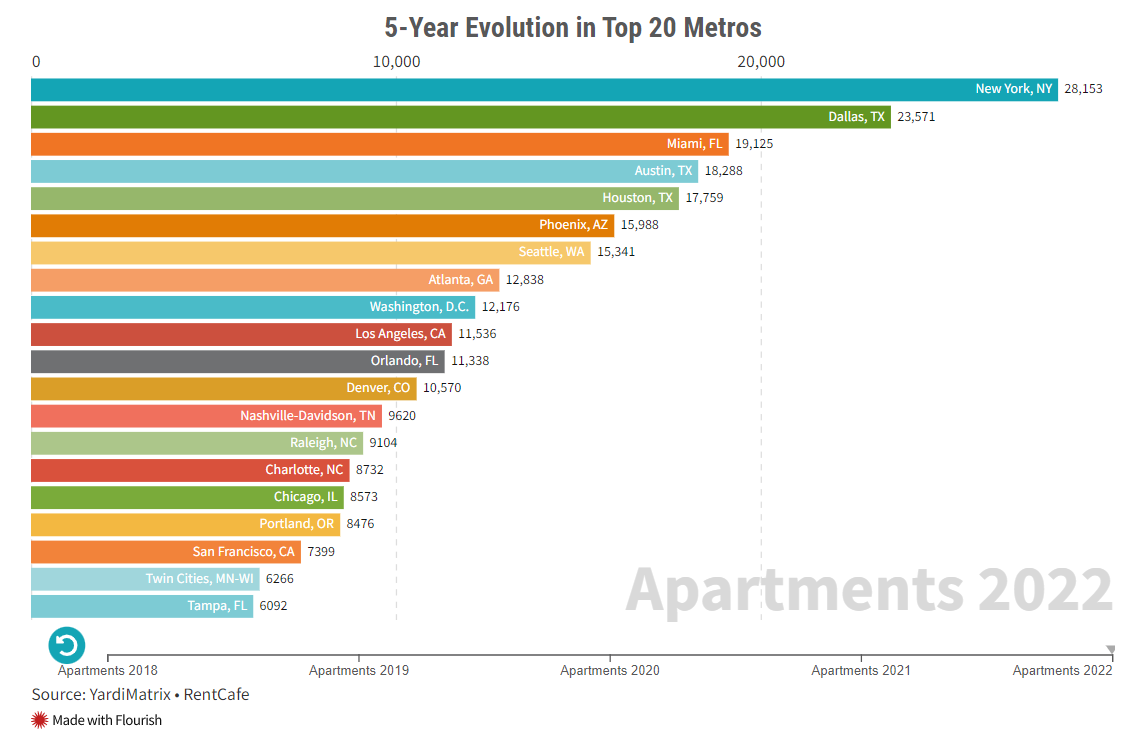

Looking nationally, the New York metro supplanted Dallas and climbed into top spot, with more than 28,000 apartments expected in 2022. Apartment production slowed in Dallas, but the metroplex was still pumping out enough Texas Doughnuts to claim the second spot, with more than 23,000 apartments added. Posting another big year and a five-year high of 19,125 apartments added, Miami catapulted into third place.

Three more Sun Belt metros — Austin, Houston, and Phoenix — grab the next three spots, and then Seattle slots in at seventh as one of the only other northern city in the top ten. Atlanta, D.C., and Los Angeles round out the top ten. Through the first half of 2022, Seattle actually came in third, according to RentCafé, but they predict other metros will finish stronger.

“Meanwhile, the number of Seattle apartments increased by 3,232 between January and June this year to reach the third spot on our list. However, supply is struggling to keep up with demand in the Emerald City — which, like other major coastal cities, has been facing an extreme lack of housing for several years now,” researcher Veronica Grecu wrote in her post. “And, this pace of construction isn’t likely to slow down anytime soon: Seattle’s population is projected to hit 1 million by 2044 and city officials are already working on updating the One Seattle Plan that also tackles new strategies to add more housing.”

National apartment production at 50-year high

The last time the U.S. was producing as many new apartments as it is now is in 1972 when builders completed 464,000 apartments, according to Yardi Matrix figures. Of course, back then the national population was 210 million instead of 332 million, so the population-adjusted apartment production was much higher back then.

Despite the boom, construction industry analysts continue to warn of headwinds and the possibility of another major slowdown.

“The construction industry is finally returning to pre-pandemic levels of activity but is still being hampered by three familiar challenges: labor shortages; material costs and availability; and supply chain issues,” said Doug Ressler, manager of business intelligence at Yardi Matrix in a statement.

Languishing apartment production over much of the 1990s and 2000s goes a long way toward explaining the current housing affordability crisis nearly all corners of the country finds itself in the midst of now. Suburban sprawl composed mostly of federally-subsidized single-family homes became the overwhelmingly favorite housing product. The results proved disastrous for housing affordability, environmental degradation, traffic congestion, climate emissions, livability, and ultimately economic vitality and stability. With limited apartment options available, the leap to home ownership became all the more attractive, which ended up feeding into the 2008 Housing Crash, as unscrupulous banks took advantage of the desperation of prospective homebuyers with toxic loans.

If only we built more high-quality multifamily residences close to job centers our cities would be more durable and sustainable. While apartment building is up, it’s likely not up enough to correct a deeply flawed housing market or replace the copious single family housing construction that used to soak up the demand before the crash tightened up liquidity.

Hurdles to housing production remain

Even now with building setting a 50-year high, it’s still not enough apartments to keep housing prices in check, and too little housing subsidy and stabilization programs exist to ensure everyone is stably housed. As apartment production has picked up, single-family housing has continue to lag since the 2008 crash and the breakneck sprawl-building years that preceded it. The backlog of housing demand is too great for a few boom years to solve, which is why local governments must forge ahead and produce more housing at all income levels.

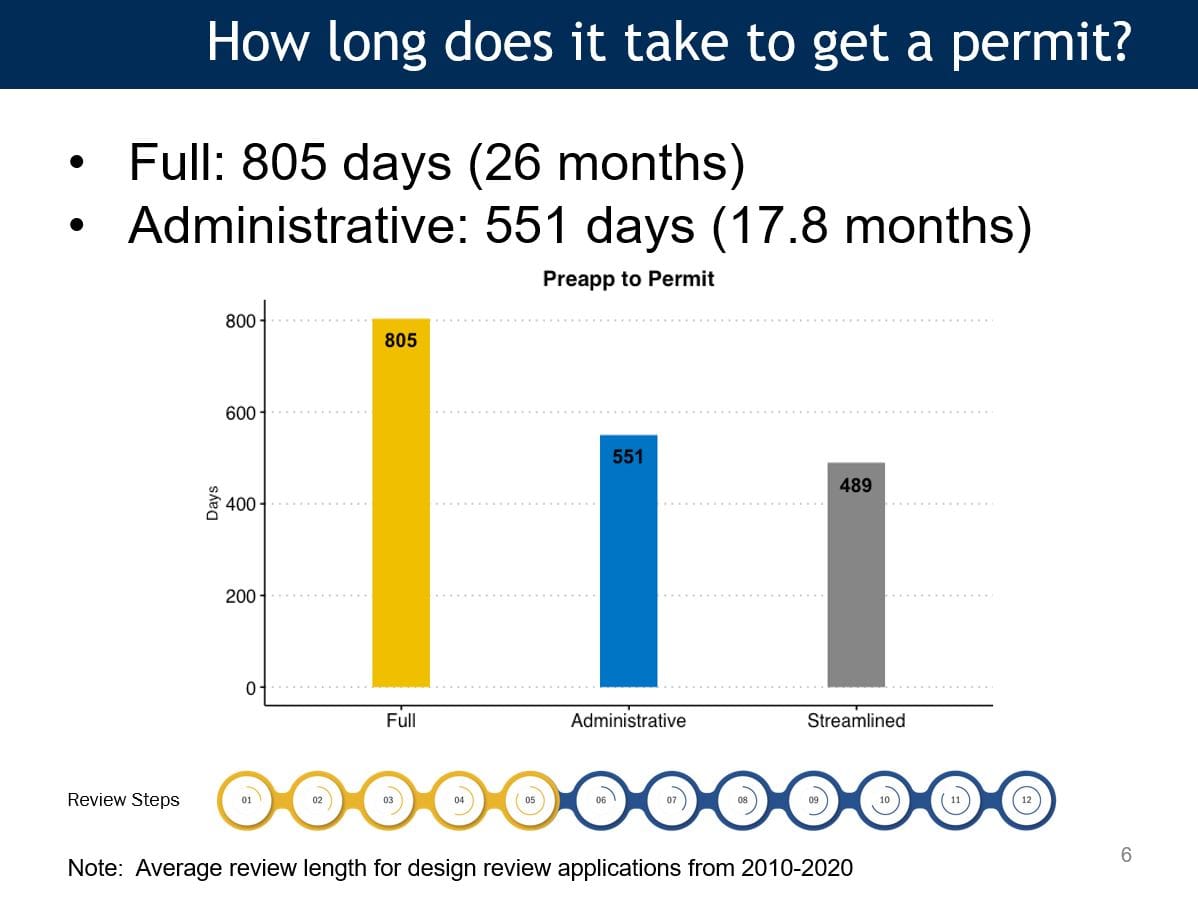

The Seattle metro set a five-year high in apartment production even with many cities sitting it out and blocking new multifamily housing starts in their midst by a variety of means, ranging from outright multifamily moratoriums (see: Mercer Island) to restrictive zoning to permitting hurdles to onerous parking requirements (see: Kirkland) to steep development fees (see: Federal Way). Seattle continues to lead the region by far even with a design review and permitting system that is direly in need of massive overhaul.

Average permitting times have steadily climbed to exceed two years in Seattle, with many unpredictable hurdles and added costs worked into the system. And still developers choose to build in Seattle, which suggest two things: Demand for living in Seattle is very high, and many Puget Sound jurisdictions aren’t much better when it comes to creating conducive conditions for homebuilders.

Seattle is in the midst of reviewing and ostensibly reforming its design review process via an official stakeholder group requested by the Seattle City Council and backed by the Harrell Administration. A coalition of housing advocates spearheaded by Seattle For Everyone (which included The Urbanist) pushed for this step, but things have not gone according to plan.

Unfortunately, the Seattle Department of Construction and Inspections (SDCI) appears intent on fighting and delaying reform rather than embracing it, and, relatedly, the SDCI-led stakeholder process has been halting, unfocused, and behind schedule so far. This has led four stakeholders to threaten to resign and the Seattle For Everyone coalition to urge the City move up its timeline and offer design review reform legislation this year rather than stringing out the process.

Meanwhile, the City is also contemplating zoning reforms with its Comprehensive Plan Update (due in 2024) that could scale back apartment bans and open up more parts of the city to “missing middle” housing growth — and potentially more mid-rise and high-rise housing, too.

It turns out the Seattle process to reform the Seattle process is also itself a slow Seattle process. Have we entered a time loop? To make matters more difficult, the editorial board from the paper of record in this region will fight it every step of the way. But Seattle certainly should see through reforms and outright overhauls to ensure the city can grow equitably and not lock out generations of residents from living in this city without being a millionaire.

It’s Time to Overhaul Design Review

Apartment Production Declines toward a 5-Year Low in Seattle Metro

{kind=link}